Upcoming Event

Free Newsletter

Free Newsletter

(Photo/DepositPhotos)

(Photo/DepositPhotos)

War takes its toll but relief is in sight

Stephen Slifer // June 5, 2026//

- A tentative U.S.-Iran ceasefire extension could help lower oil and gasoline prices.

- Falling energy costs may reduce inflation to around 2.5% by year-end, according to the analysis.

- Lower inflation could push bond yields and mortgage rates lower in the coming months.

- Economic prospects for the U.S. and global markets remain closely tied to developments in the conflict.

The U.S. and Iran appear to have reached a tentative deal to extend the ceasefire for another 60 days.

The U.S. and Iran appear to have reached a tentative deal to extend the ceasefire for another 60 days.

According to news sources Iran would have to remove all mines from the Strait of Hormuz within 30 days. In exchange the U.S. would gradually lift its naval blockade on Iranian ports which would allow Iran to sell more oil.

That would be an unambiguously positive event. Oil and gasoline prices have already fallen sharply. The stock market climbed to yet another record high level. The inflation rate would soon begin to decline.

Once inflation begins to subside long-term interest rates would begin to decline as would the 30-year mortgage rate. This good news depends crucially on reaching an agreement which we think will happen. It is in the interest of both sides to do so. The U.S. has its mid-term election coming up in November. Trump and the Republicans do not want the war to still be an issue during the summer months leading up to the election.

Once inflation begins to subside long-term interest rates would begin to decline as would the 30-year mortgage rate. This good news depends crucially on reaching an agreement which we think will happen. It is in the interest of both sides to do so. The U.S. has its mid-term election coming up in November. Trump and the Republicans do not want the war to still be an issue during the summer months leading up to the election.

The Iranians need to sell more oil to rebuild their country and, potentially, restart their nuclear program. Lots of issues must still be resolved, but a continuation of the cease fire is a significant step in the right direction.

The Iranians need to sell more oil to rebuild their country and, potentially, restart their nuclear program. Lots of issues must still be resolved, but a continuation of the cease fire is a significant step in the right direction.

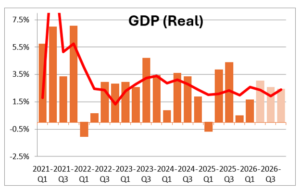

GDP growth in the first quarter was trimmed by 0.4% to 1.6%. The war that began on Feb. 28 undoubtedly took its toll on growth in that quarter.

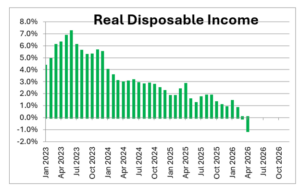

Real disposable income has declined in each of the past three months and has fallen 1.1% in the past year as the run-up in inflation has reduced consumer purchasing power.

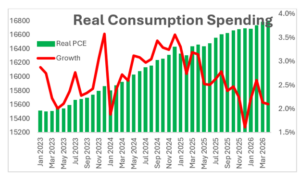

Middle- and upper-income consumers still seem willing to dip into their stock market gains and spend at a moderate 2.1% pace to maintain their lifestyle, but lower income consumers are struggling. With real income now declining one wonders how much longer middle- and upper-income consumers are willing to ignore the drop in their purchasing power.

Middle- and upper-income consumers still seem willing to dip into their stock market gains and spend at a moderate 2.1% pace to maintain their lifestyle, but lower income consumers are struggling. With real income now declining one wonders how much longer middle- and upper-income consumers are willing to ignore the drop in their purchasing power.

Mortgage rates remain around 6.5% which is preventing what appeared to be an incipient recovery in housing at the beginning of the year when mortgage rates dipped briefly to the 6.0% mark. The rebound to 6.5% mortgage rates quickly snuffed out that hint of a rebound.

An extended cessation of the fighting in Iran would, at a minimum, reduce oil prices. WTI crude oil has already declined more than 20% from a peak of $115 per barrel to $88. Admittedly, prices would remain far above the $65 per barrel price that existed prior to the war, but a 20% drop would be significant. Wholesale gasoline prices have fallen by a roughly comparable amount.

An extended cessation of the fighting in Iran would, at a minimum, reduce oil prices. WTI crude oil has already declined more than 20% from a peak of $115 per barrel to $88. Admittedly, prices would remain far above the $65 per barrel price that existed prior to the war, but a 20% drop would be significant. Wholesale gasoline prices have fallen by a roughly comparable amount.

A 20% drop in energy prices in the next couple of months could reduce both the overall CPI inflation rate and the core rate to about 2.5% by the end of the year.

Such a slowdown in inflation should allow bond yields to fall from about 4.5% currently to perhaps 4.0% by year-end.

That would, in turn, reduce the 30-year mortgage rate from 6.5% or so currently to perhaps 6.0% by year-end.

Lower rates and reduced inflation would power the stock market to even higher prices.

It is not clear whether 2.5% GDP growth in the second half of this year, an unemployment rate that remains at 4.3% which is essentially its full employment threshold, and a 2.5% core CPI inflation rate would be enough to get the Fed to cut rates. We suspect that it will not reduce rates between now and yearend, but there is a new Fed chair who is so inclined. We should learn more about his intentions following his first FOMC meeting on June 16-17.

The point of all this is that the outlook going forward depends largely on the outcome of the war. An extension of the cease fire is an important ingredient. We have seen in the stock, bond, and oil markets the positive impact it would have on the economic outlook for the United States, and it would do the same thing for other countries around the globe.

From 1980 until his retirement in 2003, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.